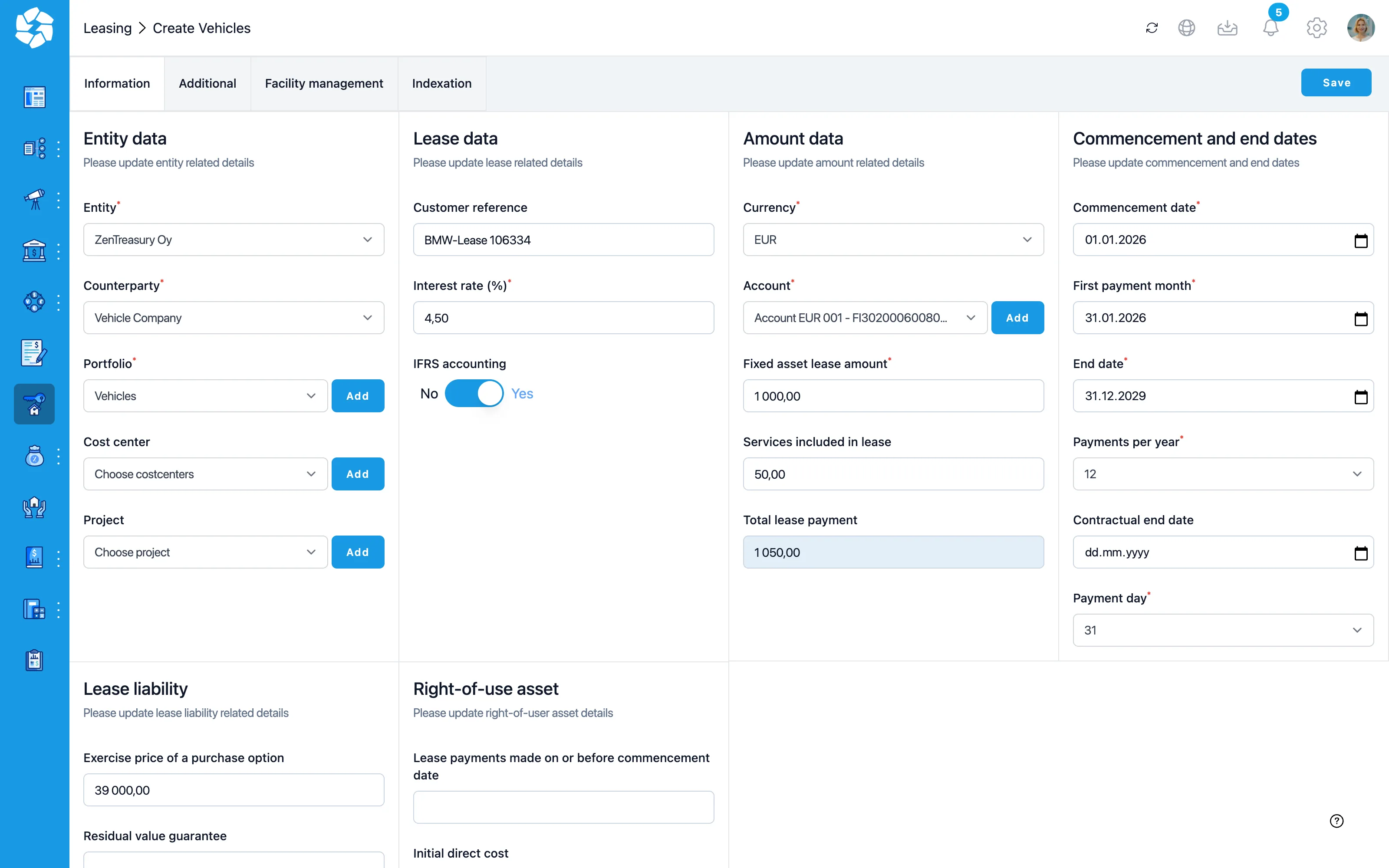

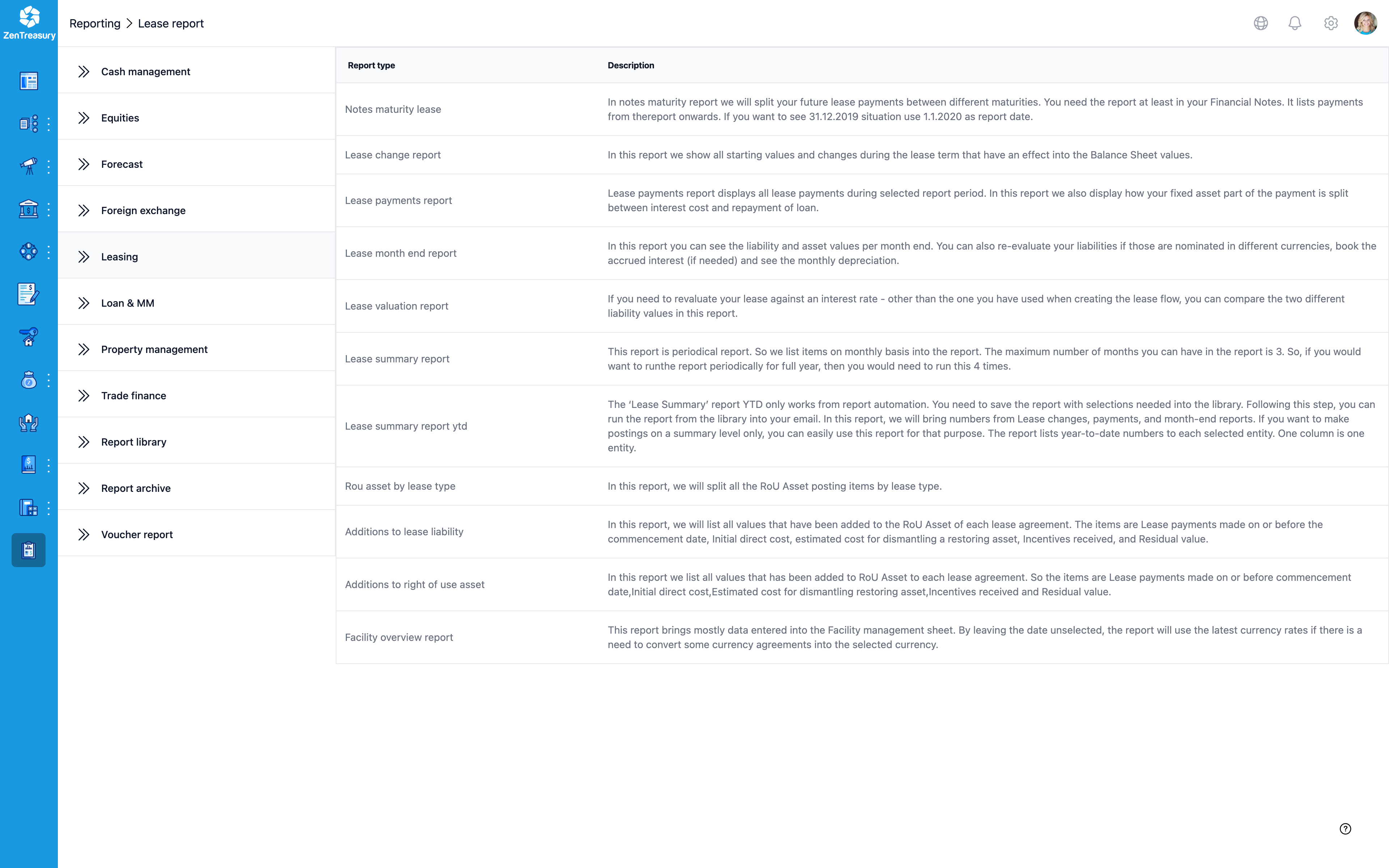

Indexation clause

Event

The landlord exercised an annual indexation clause. Payment goes from €10,000 to €11,000.

What the ERP records

Recurring payment amount changed.

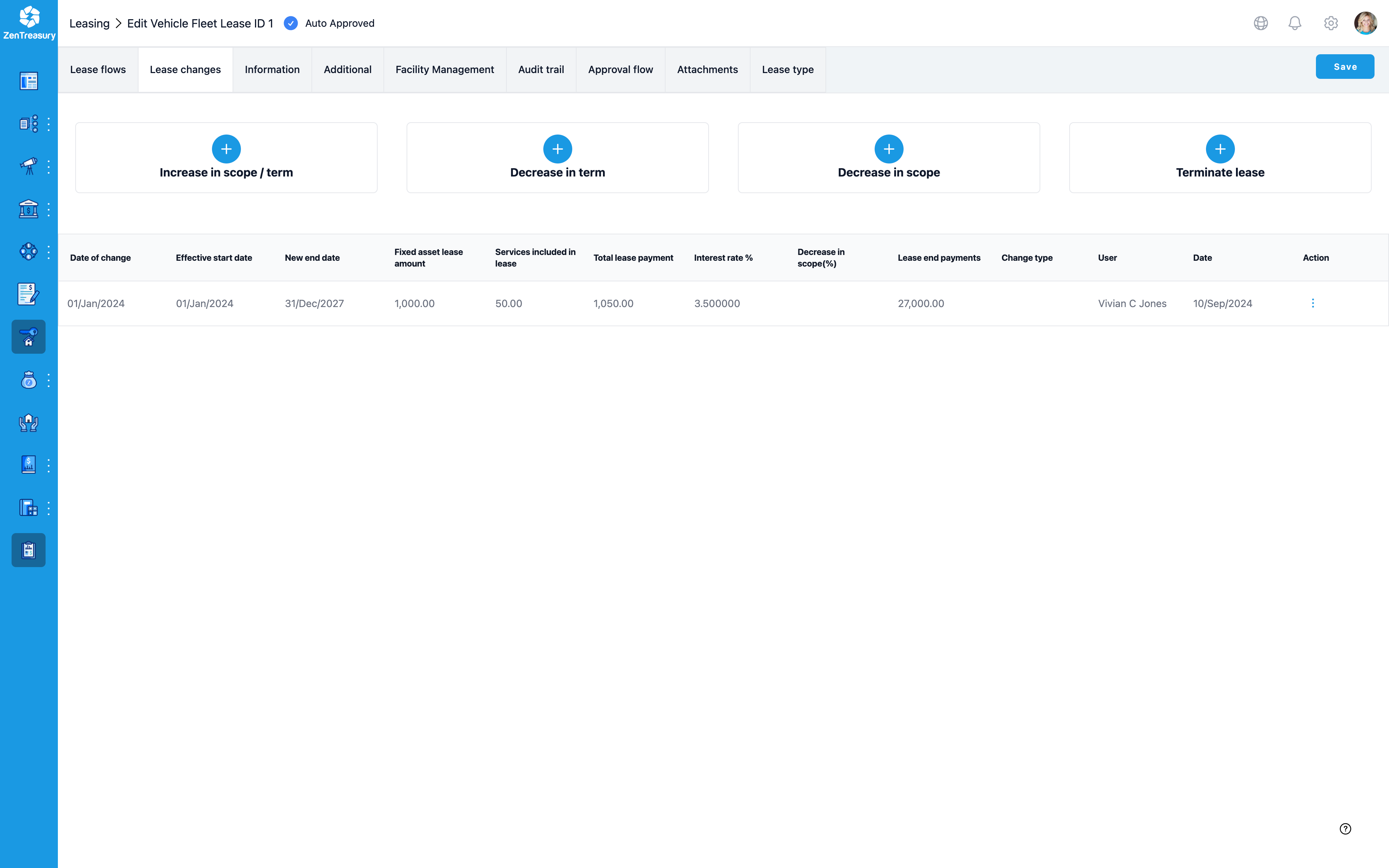

What IFRS 16 requires

- Remeasure the lease liability using the original discount rate.

- No adjustment to the right-of-use asset depreciation schedule.

- Adjustment posts to lease liability and P&L.

| Period | Liability | Δ |

|---|---|---|

| Before | €248,500 | 0 |

| After | €256,400 | +€7,900 |